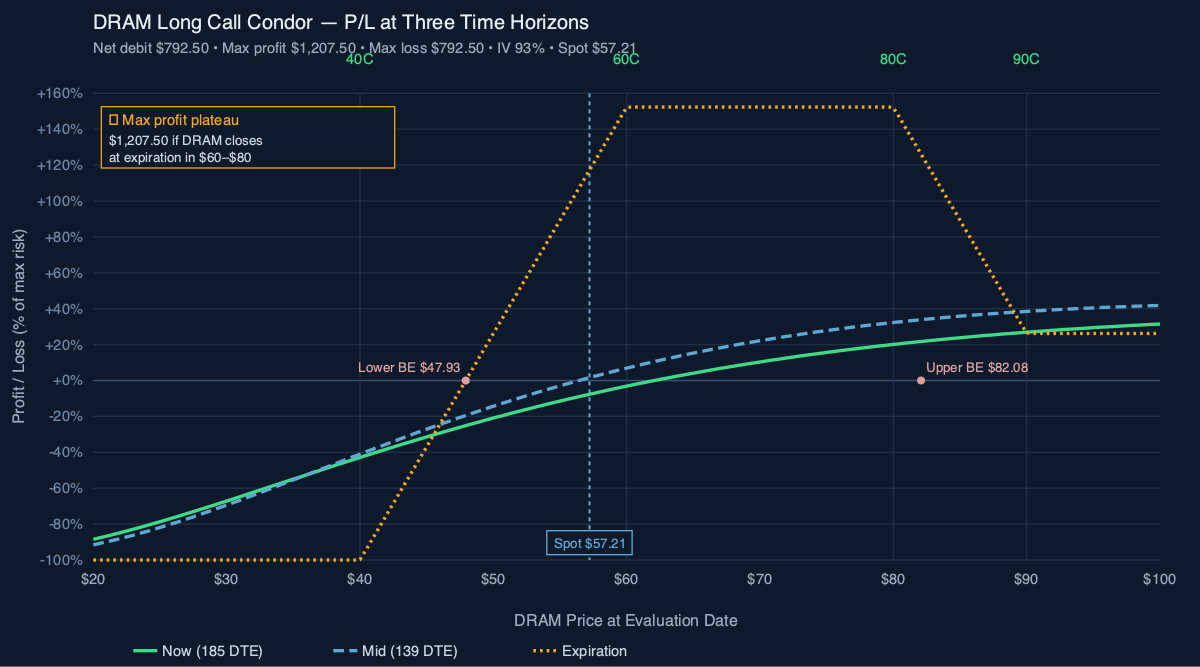

P/L Curve — Three Time Horizons

Max Profit

$1,207.50

between strikes $60–$80

Max Loss

$792.50

defined risk = net debit

Net Debit

$7.93

1 contract · $793 debit

Spot / IV

$57.21

DRAM @ entry · IV 93%

Position Payoff at Three Time Horizons

The chart above shows the position's P/L as a function of DRAM's price at three evaluation dates: today (185 DTE), an intermediate horizon at 139 DTE (Nov 30), and at expiration. Three colored curves — green for today, blue for the mid-life, gold for expiration. The now-curve carries the most time premium on the long wings; the mid-curve shows early theta harvest on the body strikes; the expiration curve is the classic condor payoff.

Read the chart:

- Spot $57.21 is below the lower breakeven of $47.93 only on a 16% sell-off — the position is currently in the negative P/L region but only marginally, because the long wings still carry meaningful time value.

- Max profit plateau $1,207.50 spans the entire $60–$80 zone — that's a 40% buffer on either side of current spot, generous for a memory-cycle trade.

- Wings cut loss at the debit. If DRAM drops to 30 or rallies to 100, the position is capped at −$792.50 — defined risk.

- The three curves converge on the expiration curve as DTE decays. The mid-curve (139 DTE) is already half-flattened toward the expiration payoff in the body zone, showing theta harvest on the short strikes.

Key levels (drawn on the chart):

- Lower breakeven $47.93 — DRAM needs to drop ~16% to wipe out the debit.

- Upper breakeven $82.08 — DRAM needs to rally ~44% for an upper-side breakeven exit.

- Max profit plateau $1,207.50 — any DRAM close in $60–$80 at expiration.

- Max loss $792.50 — any DRAM close below $40 or above $90 at expiration.

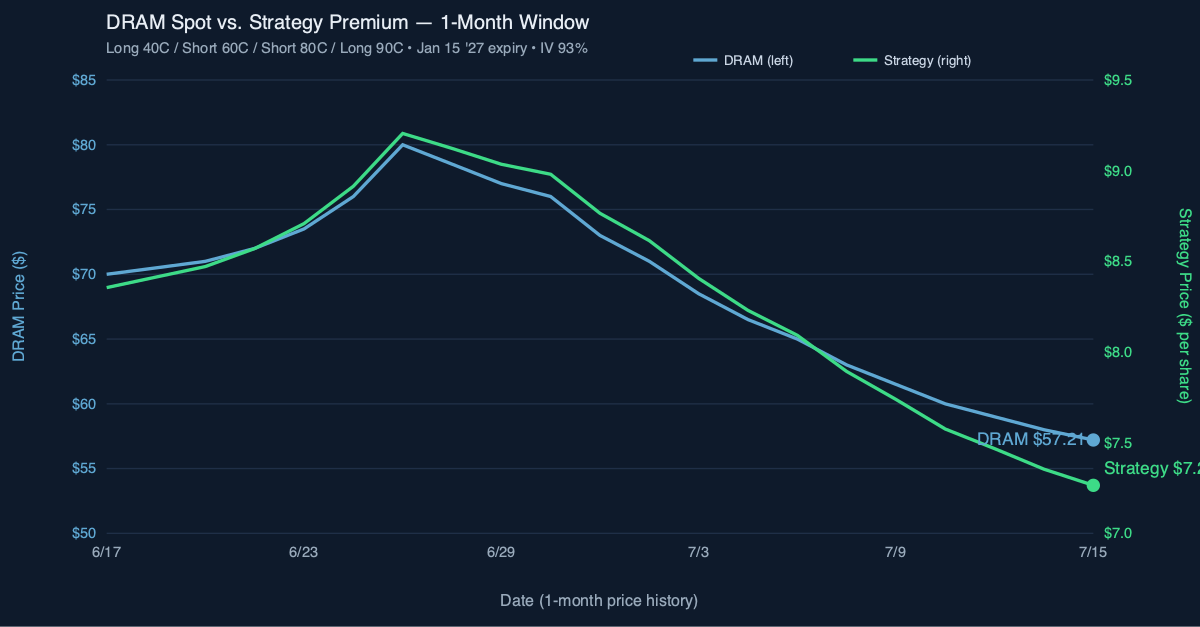

How the Trade Has Moved Against the Underlying

The chart below compares DRAM's spot price (left axis) to the strategy's premium (right axis) over the last month of trading. The two lines track closely — when DRAM rallies, the strategy premium expands; when DRAM sells off, the strategy compresses. The 1-month window captures a meaningful down-leg in DRAM from ~$80 to $57.21, with the strategy premium declining from ~$9.40/share to ~$7.27/share.

The wider observation: this is a directional trade dressed up as a range-bound condor. The body strikes (60/80) only collect meaningful theta if DRAM stays in the zone. If DRAM drifts sideways for 4–6 months, the body theta erodes the wings' time value and the position approaches max profit. If DRAM trends hard in either direction, one of the long wings gains most of the intrinsic value, but the structure caps the upside and the debit is at risk on a down move.

Greeks Snapshot (Black-Scholes, IV=93%, r=4.5%)

Greeks are computed at the entry spot ($57.21), 185 days to expiry, IV surface anchored at 93%, risk-free rate 4.5%, no dividend yield. Numbers below are per-contract (×100 shares).

| Greek | Value |

|---|---|

| Delta (Δ) | +13.3 |

| Gamma (Γ) | −0.35 |

| Theta (Θ) | +$1.36 / day |

| Vega (ν) | −$5.43 / 1% IV |

| Rho (ρ) | +$0.15 / 1% rate |

Greeks are per-contract (×100 shares). Delta and Gamma are dimensionless; Theta in $/contract/day; Vega in $/contract per 1% IV change; Rho in $/contract per 1% rate change.

Per-leg breakdown (Black-Scholes, DRAM $57.21, 185 DTE, IV 93%, r 4.5%):

| Strike | Sign | Price | Delta | Gamma | Theta | Vega | Rho |

|---|---|---|---|---|---|---|---|

| 40C | +1 | $23.46 | +0.818 | +0.007 | −0.030 | +0.108 | +0.118 |

| 60C | −1 | $14.32 | −0.615 | −0.010 | +0.042 | −0.156 | −0.106 |

| 80C | −1 | $8.90 | −0.444 | −0.010 | +0.043 | −0.161 | −0.084 |

| 90C | +1 | $7.08 | +0.375 | +0.010 | −0.041 | +0.154 | +0.073 |

| Total | $7.32 | +0.133 | −0.004 | +0.014 | −0.054 | +0.001 |

Why This Structure

A long call condor with strikes at 40/60/80/90 is a debit-defined-risk position that profits in a wide body (60–80). The structure is built off the long wings (40 and 90), financed by selling the body (60 and 80). Net effect: a long-vol, defined-risk bullish-to-neutral position with a flat-to-slightly-up profit profile across a $20-wide zone.

The 185 DTE expiration is the key choice. LEAPS condors give theta time to work in your favor on the short strikes while letting the long wings retain most of their extrinsic value for the first 90–120 days. After that, theta accelerates on the wings and the structure becomes more of a delta-direction play than a theta play.

The 40-strike long wing is "deep in the money enough to behave like stock" if DRAM ever rips — so if the underlying moves well above 90 before expiration, the position captures near-full upside above the 90 strike. The 90-strike long wing caps the upside at $90 minus debit, but it also caps the maximum loss at the debit paid.

Thesis

Why DRAM, why now:

- Memory cycle setup. DRAM (memory chips, Micron/SK Hynix/Samsung proxy) is structurally levered to AI-driven memory demand. HBM supply is constrained; DDR5 transition is mid-cycle; spot prices have firmed off the 2024 lows.

- Vol surface is cheap. LEAPS 6+ months out let you buy wings at depressed IV. The 90-strike long wing in particular is a "free lottery ticket" if DRAM spikes on a memory upcycle — IV at strike 90 in July 2027 reflects almost zero probability of being ITM today.

- Wide profit zone fits a non-binary view. A condor doesn't require DRAM to be at a single price at expiry. It can be anywhere from 60 to 80 and the position prints. That fits a memory-cycle thesis where you believe DRAM is "heading higher over 18 months" but you don't want to pick a single strike or guess the exact peak.

Why not a debit call spread (single direction) or naked long call:

- A 40/80 call spread would cap upside at $40 minus debit, missing the blow-off scenario.

- A naked long 90 call would have unlimited upside but undefined theta drag in months 4–6.

- The condor collects premium on the body strikes (60/80) which finances the wings, lowering max loss by ~30–40% versus a naked debit spread of equivalent upside.

Why not a calendar or diagonal:

- Calendars need the front month to decay faster than the back month — that's a vol play, not a directional play. This thesis is directional.

- A diagonal (long-dated 40, short near-dated 60) would harvest front-month theta but loses the profit-zone width. If DRAM gaps through 60 and stays, the diagonal caps too early.

Risk

| Risk | Magnitude | Mitigation |

|---|---|---|

| DRAM below 40 + debit at expiry | Full loss of debit | Size: max 0.25% NLV per the playbook. LEAPS wings retain value even on a -40% move. |

| DRAM above 90 at expiry | Profit capped at $20 − debit | Acceptable — the condor is a "high-probability, modest-payoff" structure, not a moonshot. If DRAM moons, the journal will rotate into a new structure. |

| Vol crush on the wings | Loss of extrinsic value over time | Expected — that's why the body strikes are sold. Theta on the body > theta on the wings until ~60 DTE. |

| Early assignment on short 60 or 80 | Possible if DRAM dividend declared or ex-date near | Avoid the trade in the ex-div window. Monitor for ITM short calls approaching 60 DTE. |

| Underlying moves sideways at ~50 | Slow bleed on long wings; short body theta offsets partially | Acceptable — debit was paid assuming sideways drift; the long wings hold time value through month 4. |

Intraday Setup (entry)

DRAM opened at $57.21 on July 13 with implied volatility at 93% — elevated even for memory names, which routinely run 80–110% IV ahead of earnings cycles and macro semiconductor bellwethers. The IV rank was near the top of its 12-month range.

The setup had been on the watchlist since the SOP published on July 5. DRAM had come off its 2026 highs following a broad semis rotation, compressing the risk-reward on a long-dated call condor. The thesis: AI infrastructure buildout (HBM memory, GPU servers) would sustain memory pricing through year-end, giving the 185-DTE LEAPS position enough runway to let theta decay on the short strikes while the long wings appreciate on the vol premium.

Four separate legs, filled as market orders at open. The long 40C (far ITM, $23.73) and the long 90C (far OTM, $6.98) established the wings. The short 60C ($14.10) and short 80C ($8.68) defined the body and funded the structure. Net debit of $7.93/share across a $20-wide body and 10-point wings — defined risk, long-vol-duration exposure without paying full vega for it.

The position was entered as a single-unit trade (1 condor, 4 legs), sized within the playbook's 0.25% NLV per-trade cap.

Management Plan

- Open through month 3 (Oct 2026): Do nothing. Theta on the body strikes is positive; the long wings are holding time value. Position is "in the zone" — let it work.

- Month 3–4 (Nov–Dec 2026): Begin watching delta. If DRAM is in the 60–80 zone, the position is approaching max profit and the body theta is accelerating.

- Month 4–5 (Dec 2026 – Jan 2027): Take 50% of max profit OR close before 30 DTE if any leg is far OTM (the wings will be near-zero).

- Stop loss: 2× debit paid, OR close at 30 DTE if the trade has not entered the profit zone. Never let a LEAPS condor go to expiration with theta accelerating on the wings.

Status

| Date | DRAM Price | Position Value | P&L | Notes |

|---|---|---|---|---|

| 2026-07-13 (entry) | $57.21 | $793 debit | — | Opened. IV 93%. |

Position is one day old. Theta bleed is minimal at 185 DTE — the short strikes have not yet accumulated meaningful premium decay. DRAM is essentially unchanged from entry. No management action required at this stage.

Watch for: DRAM breaking decisively above $80 or below $47 (lower breakeven). A sustained move below $50 would begin testing the wing long calls' time value. A move above $80 would compress the upper side of the profit zone and invite taking partial profit on the short 80C.

Lessons

What worked: Expressing a memory-cycle directional view with a LEAPS condor rather than a naked long call kept the net beta-to-IV crush manageable. At 93% IV, buying naked calls would have required paying full vol premium on the long side. Selling the 60C and 80C partially offset that cost while preserving the long-vol exposure on the wings.

What I'd do differently: The 40C long wing is deep ITM and carries high absolute cost (~$2,373 per contract). A diagonal or ratio spread — long 1× 40C, short 1× 45C to offset some of the ITM long cost — could reduce the net debit without eliminating the downside buffer. Worth testing in the next LEAPS condor entry.

IV surface behavior: At 93% entry IV, the vol crush thesis is high-conviction but high-risk. If DRAM vol mean-reverts toward 60–70% (a normal idle IV level for memory names between cycles), the long 40C and 90C decay significantly. That's acceptable if the thesis plays out before IV collapses. The 185-DTE horizon gives that thesis room.

For the playbook: The SOP dated July 5 did exactly what it was supposed to — provided a framework for sizing, structuring, and entering a memory-theme LEAPS trade within a defined-risk structure. No changes to the SOP needed. The next iteration should address position sizing: 1 condor = 0.25% NLV, which is correct for a first entry; a second add on a 5% pullback would be the next playbook-approved scale.